2025 IFRS example sustainability disclosures

ESG and sustainabilityExplore IFRS 2025 example sustainability disclosures aligned with ISSB and closely to CSSB standards, and how Canadian organizations can prepare for future reporting requirements.

29 Jan 20246 min read

Many companies located in and outside of the European Union (EU) may be affected by the EU’s Corporate Sustainability Reporting Directive (CSRD). The CSRD is expected to affect up to 50,000 entities that are not currently required to report on environmental, social, and governance (ESG) activities under the EU’s Non-Financial Reporting Directive (NFRD). The phase-in period for CSRD reporting may begin as early as fiscal 2024 reporting.

The CSRD creates reporting obligations for certain non-EU parent entities with operations in the EU at both a consolidated parent and EU-subsidiary level. The CSRD requires different disclosure standards and staggered effective dates, depending upon the type of entity. Due to the layers of complexity, Canadian entities with revenue or operations in the EU are encouraged to evaluate the impact of the CSRD immediately.

The European Commission laid out its plan to transform Europe into the world’s first climate-neutral continent through a series of policy initiatives and legislative acts in its 2019 European Green Deal. A key element of climate neutrality involves shaping a green economy, which means directing public and private capital toward sustainable business.

Reporting requirements within the EU Taxonomy and the CSRD aim to improve the reliability and usefulness of sustainability information to investors, as well as combine and modernize several existing frameworks. The EU taxonomy provides clear criteria for economic activities to qualify as “sustainable,” while the CSRD greatly enhances the breadth, depth, and uniformity of the EU’s ESG and sustainability reporting ecosystem.

The CSRD replaces the EU’s existing NFRD and establishes comprehensive ESG reporting requirements within a distinct section of a management’s report.

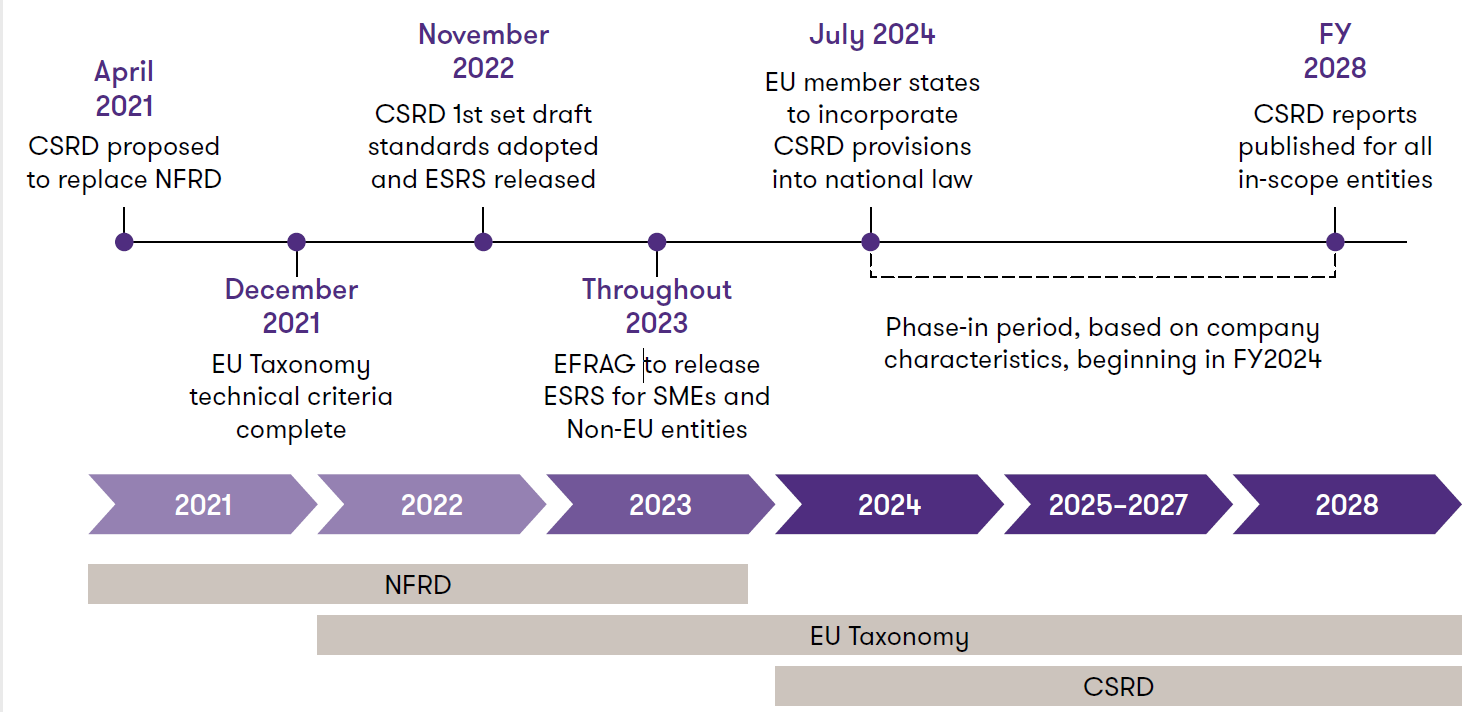

This timeline describes how the CSRD was proposed as a replacement for the NFRD in April 2021 and the major development milestones that have occurred and are expected since then.

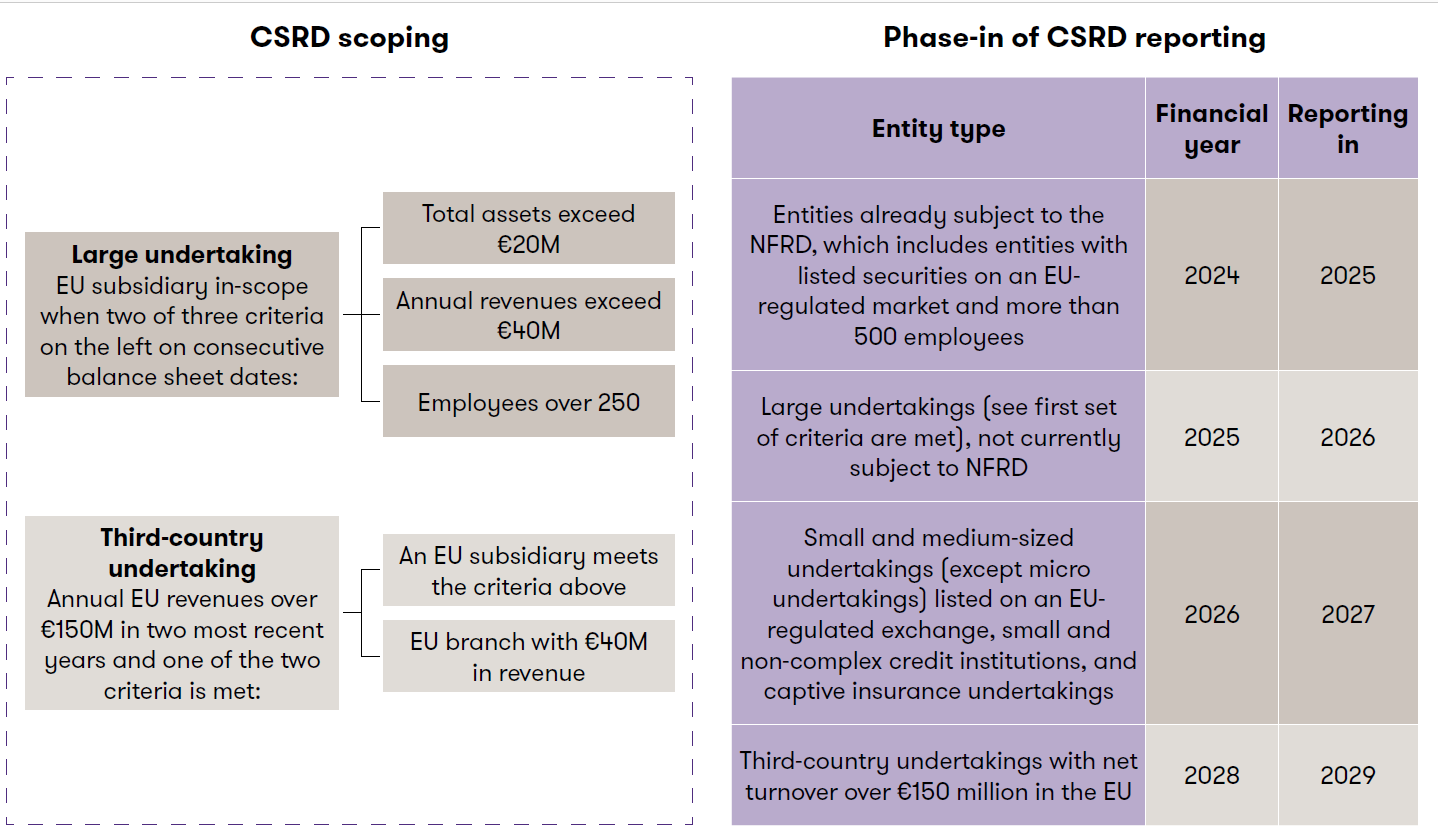

Determining whether your business needs to comply with the CSRD and when to report can be complex. The CSRD applies to:

This chart shows how CSRD reporting requirements will be phased in gradually based on the type and size of the reporting entity.

Some Canadian entities, especially those with complex legal structures or those that take advantage of parent or group consolidated or combined reporting accommodations, may benefit from working with legal counsel to understand and optimize the reporting requirements for their organizational structure.

All businesses in the CSRD’s scope are required to obtain limited assurance from a third-party verifier in their first reporting year. The European Commission is evaluating whether the need to obtain reasonable assurance is feasible and this measure may be adopted at a future date.

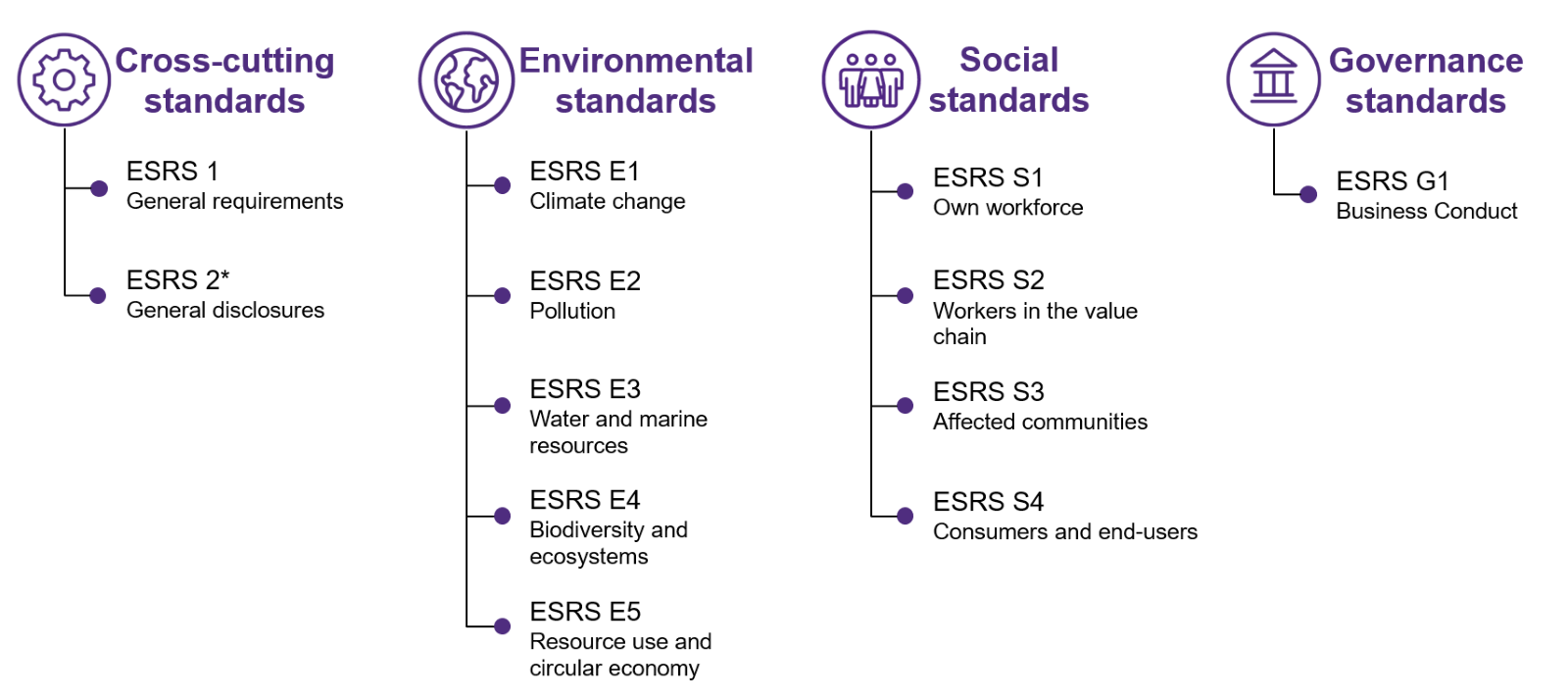

The CSRD directs the European Financial Reporting Advisory Group (EFRAG) to establish a reporting framework called the European Sustainability Reporting Standards (ESRS). The framework includes general, cross-cutting requirements that apply to all in-scope companies and topical disclosures that may or may not be material to a company. Below is a summary of the currently available standards:

These are the 12 standards released by the ESRS in November 2022. Two cross-cutting standards and ten topical (E, S, or G) standards.

Each ESRS topical standard is organized based on a uniform set of disclosure areas, including:

The ESRS will also require disclosures related to sector-specific impacts, risks, and opportunities, which are expected to be released by June 2024.

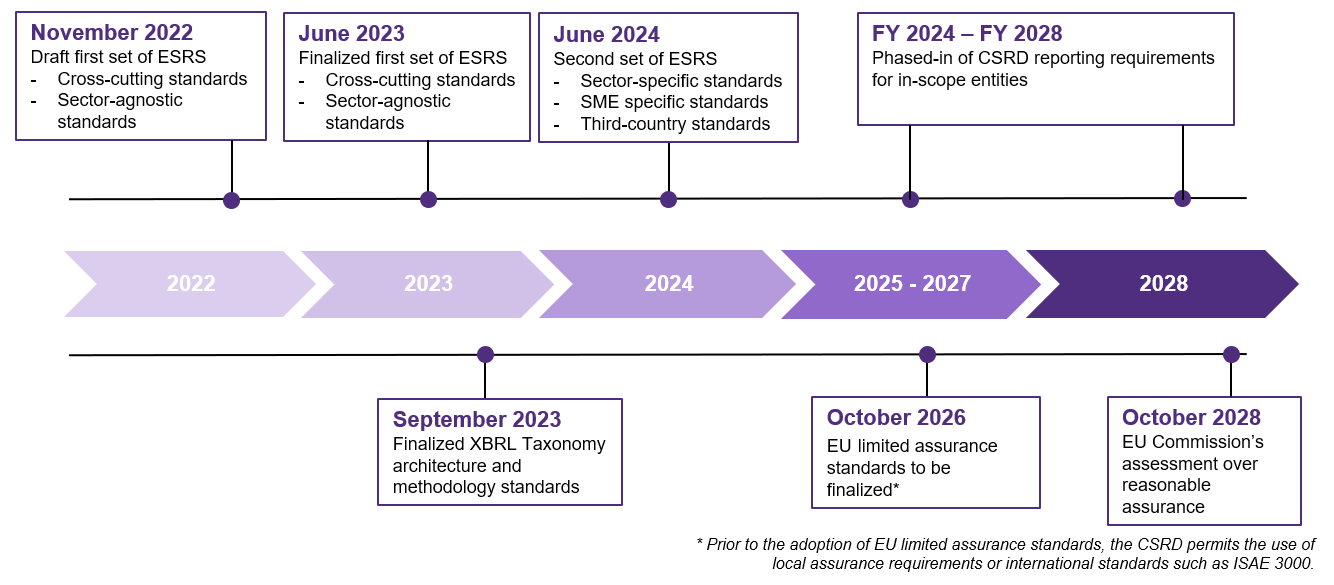

This timeline shows the expected development of the ESRS overlayed with relevant activities by the EU Commission and the CSRD reporting phase-in timeline.

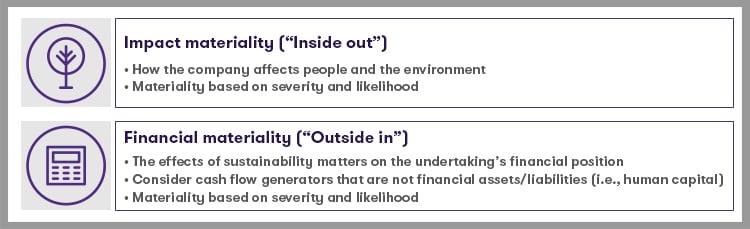

While the ESRS framework addresses several key ESG topics, only those that present material impacts, risks, and opportunities need to be included in a CSRD-compliant management’s report. The CSRD mandates that materiality be assessed through a “double materiality” lens, considering both impact and financial materiality. In addition, within its general disclosures, a company will report on how it determined its material topics.

Impact materiality

Impact materiality is known as the “inside out” approach, as it relates to the impact0 that the company has on a sustainability matter. Impacts could be actual or potential, positive and negative, over the short-, medium-, and long-term time horizons. Impacts also include those caused or contributed to by the company’s own operations, products, or services through its business relationships. Materiality is considered based on the impact’s severity (in scale, scope, and irremediable character), and likelihood.

Financial materiality

Financial materiality is known as the “outside in” approach, as it relates to the effects of sustainability matters on the company ( e.g., current or future cash flows, development, performance, position, cost of capital, or access to finance). The scope of financial materiality for sustainability reporting is broader than the scope used to determine materiality for the financial statements. Risks may include factors of value creation that do not meet financial accounting definition of assets/liabilities but contribute to the generation of cash flows or development of the undertaking. Materiality of risks is assessed based on a combination of the likelihood of occurrence and the size of the potential financial effects.

Chart shows the characteristics of impact materiality (“inside out”) and financial materiality “outside in”.

Entities are required to consider each materiality perspective individually and disclose both information material under both perspectives and information material under just one of the perspectives.

Every business’ path toward CSRD compliance will be unique based on the nature of its business, its phase-in timetable, and its current sustainability reporting status.

Canadian entities should consider taking the following next steps:

We encourage all entities that may be affected by these Standards to start to consider the impact of them now. Navigating these CSRD can be complex—but we’re here to help.

Explore IFRS 2025 example sustainability disclosures aligned with ISSB and closely to CSSB standards, and how Canadian organizations can prepare for future reporting requirements.

Our latest report explores how the mid-market is driving a more sustainable planet through continued investment and a clear strategic drive to make a change.

After the first year of reporting in 2024, there are some common misconceptions about the Modern Slavery Act and how organizations can comply. We’re addressing four myths to help you understand how these rules may affect your business in time for the 2025 reporting cycle.