What the new Canada Emergency Wage Subsidy rules means for your business

28 Jul 2020On July 17, 2020, the federal government introduced proposed changes to the Canada Emergency Wage Subsidy (CEWS) rules. Ten days later, the changes were enacted into law on July 27, 2020.

The changes significantly enhance the existing CEWS program by

- extending its availability to December 31, 2020;

- providing for a gradual reduction of the subsidy as employers’ revenues improve;

- providing those employers suffering the most with a higher subsidy for periods five and six;

- making it more likely for some owner-managers to access the program (if they were unable to under the original rules); and

- making it more accessible to a greater number of employers.

However, while these changes will introduce a host of benefits, they will also be considerably more complex than the original rules.

CEWS Extension to December 31, 2020

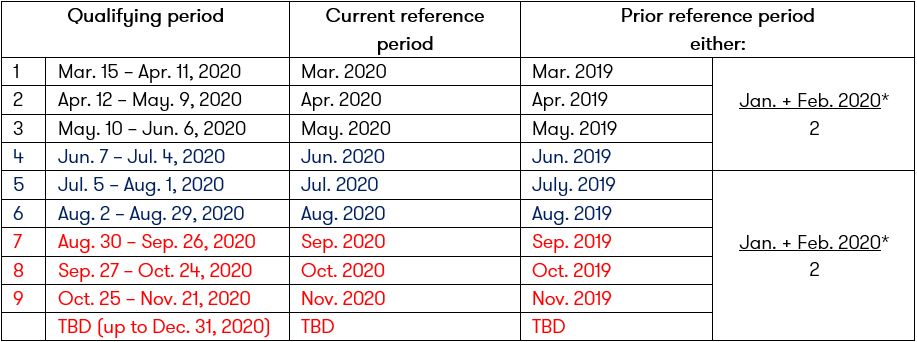

The original CEWS included three qualifying periods (noted below). It was later extended to include three more qualifying periods up to August 29. With the most recent changes, the CEWS is now extended to December 31, 2020.

Extended CEWS periods

*To use the average monthly revenue for January and February 2020 as the qualifying revenue for the prior reference period, a separate election is required for qualifying periods 1-3 and for 5-9.

Wage subsidy calculation

Starting with the fifth qualifying period (July 5 – August 1, 2020), an eligible employer that has experienced any rate of decrease in revenue in the current period (as compared to a prior period) is eligible to receive the wage subsidy.

The wage subsidy on an eligible employee’s remuneration will consist of two parts:

- Base subsidy i.e. base percentage

- Top-up subsidy i.e. top-up percentage

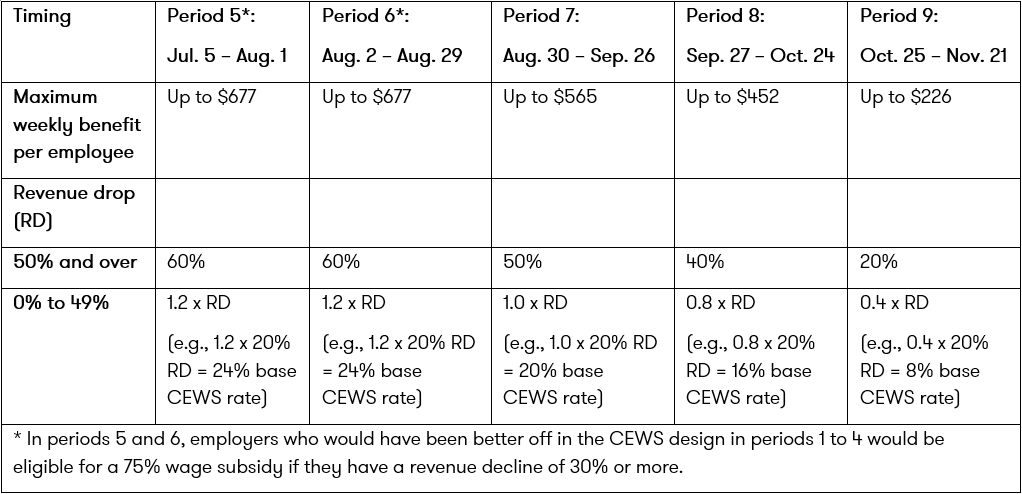

Base subsidy

The amount of the base subsidy (or base percentage) is calculated based on the rate of revenue decline, comparing the current period to a prior period (see the table above). There is a weekly maximum, per period, which decreases as the program nears its end date.

Maximum amount of the base subsidy, per qualifying period

Source: CRA backgrounder

New deeming rule

Furthermore, a new deeming rule has been introduced which is meant to prevent the employer from seeing a sudden decrease in the subsidy in the event that the rate of revenue decline in the subsequent period is much less than the current period.

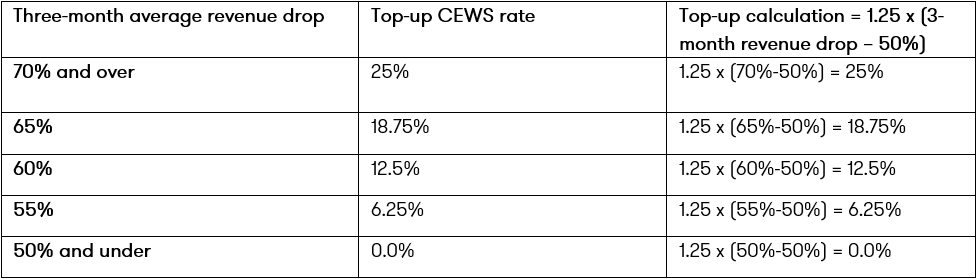

Top-up subsidy

The top-up subsidy is available to those employers that have been, according to the CRA “most adversely impacted by the pandemic” and is calculated according to the business’s drop in revenue. It compares the average monthly revenue for the three months prior to the qualifying period to either

- the average monthly revenue in the same three months of the previous year, or

- the average monthly revenue in January and February 2020.

Top-up CEWS rates for selected levels of average revenue drop over the preceding three months

Source: CRA backgrounder

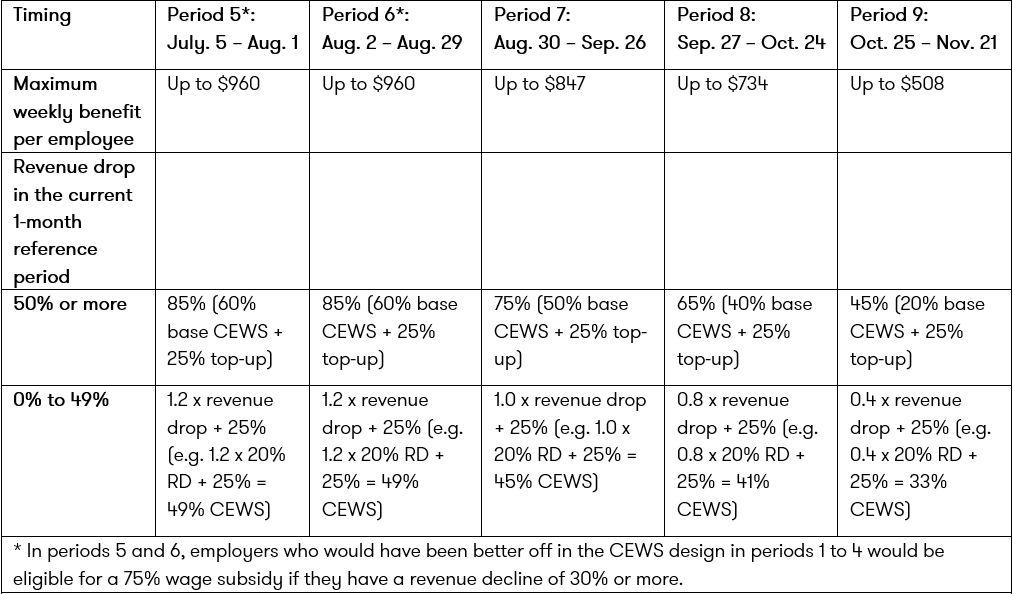

The total wage subsidy is determined by adding the base percentage and top-up percentage and multiplying the sum by the eligible remuneration paid up to $1,129. Under the original rules, the employer would multiply 75% by the eligible remuneration paid up to $1,129, yielding a maximum of $847/week. The new rules essentially change the percentage from 75% to a different percentage (although it could end up being 75%).

The rate structure of the combined base CEWS and the top-up CEWS for the most affected employers (i.e., those that experienced an average revenue drop of 70% or more in the preceding three months)

Source: CRA backgrounder

Safe harbour rule

For periods five and six, a safe harbour rule is introduced to ensure that the wage subsidy available to the employer under the new rules is not less than what it would have been under the original rules.

For these periods, any employer experiencing at least a 30% decline in revenues will determine its wage subsidy per employee as the greater of:

- 75% x the eligible remuneration paid, up to $847, or

- An amount determined under the new rules (up to 85% x eligible remuneration paid on max $1,129)

Improving access for non-arm’s length employees

Under the original rules, a non-arm’s length (NAL) employee, such as the owner of the business, who did not receive remuneration during the period January 1 – March 15, 2020 (i.e., the baseline remuneration period) was unable to access the CEWS on their own pay during the pandemic. The changes to the rules attempt to address this issue.

Employers are now able to select their baseline remuneration period, as either:

- January 1, 2020 – March 15, 2020 (as per original rules), or

- Depending on the qualifying period (QP):

- QP1 – QP3: March 1 – May 31, 2019

- QP4, either:

- March 1 – May 31, 2019, or

- March 1 – June 30, 2019

- QP5 – QP9+: July 1 – December 31, 2019

This may allow NAL employees who may not have received pay during January 1 – March 15, 2020 to receive the wage subsidy if they did receive pay during a different baseline period, as noted above.

Other changes

Other significant changes have been included, such as:

- Employers that have made business acquisitions through asset sales can qualify

- Employers using third-party payroll providers (paymaster arrangements) can qualify

- Employers that have undergone amalgamations or windups can qualify

- Employees that have not received remuneration for 14 or more days in the qualifying period can now qualify (starting with qualifying period five)

- Applicants now have the ability to elect either the cash method or the accrual method for all qualifying periods

- Applicants now have the ability to request the CRA to evaluate their CEWS claim, at any time, through a notice of determination

We are here to helpWe understand that you want to be agile and responsive as the situation unfolds. Having access to experts, insights and accurate information as quickly as possible is critical—but your resources may be stretched at this time. We’re here to support you as you navigate through the impacts of coronavirus on your business and your investments. |