Federal government changes seek to expand and extend relief

The federal government made several tax changes in recent weeks, to provide COVID-related economic relief to small businesses and employers.

These changes include:

- Expansion of the Canada Emergency Wage Subsidy (CEWS) program to make it easier for employers to qualify;

- Extension of the deadline to apply for the Canada Emergency Business Account (CEBA);

- Extension of the Canada Emergency Commercial Rent Assistance (CECRA);

- Extension of the income tax payment deadline to September 30;

- Extension to the Canada Emergency Response Benefit (CERB) as well as proposed changes after the CERB program expires.

In addition, the federal government expanded the T4 reporting requirements, adding new categories of information that employers must disclose.

The government might potentially allow employees to deduct home office expenses, but more details are expected on this point.

CEWS changes

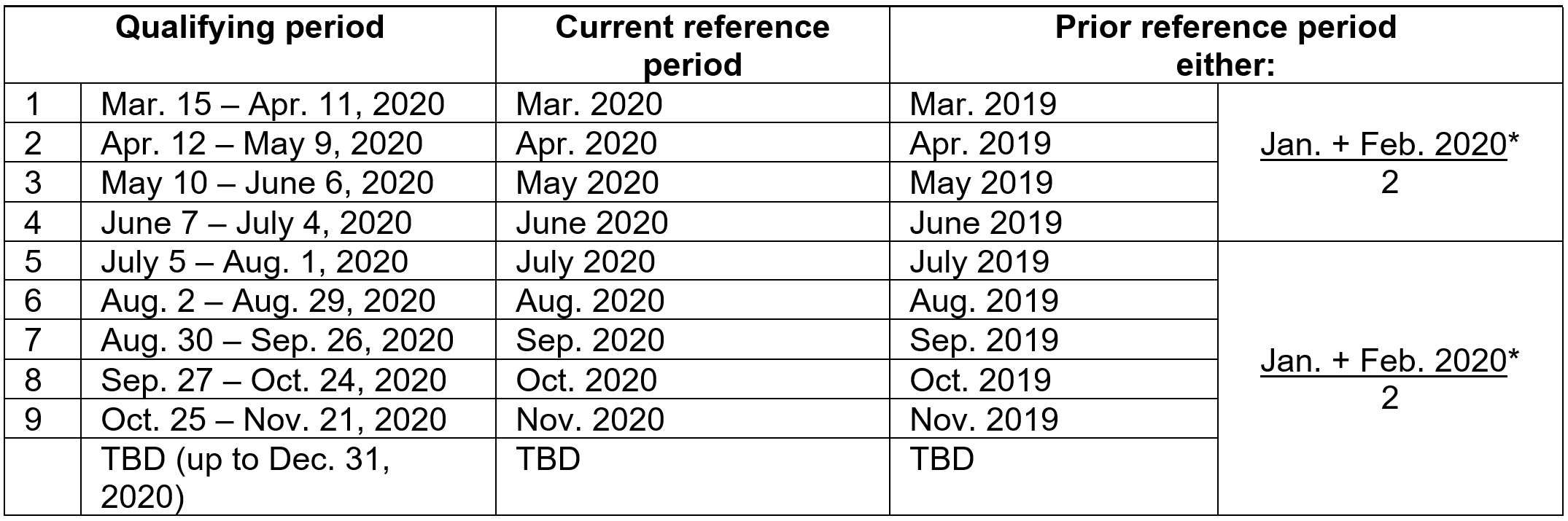

There have been several significant changes to the CEWS program. First, the program has been extended to a total of nine claim periods, the last of which ends on November 21, 2020. It can be further extended to December 31, 2020.

CEWS periods

![]()

*To use the average monthly revenue for January and February 2020 as the qualifying revenue for the prior reference period, a separate election is required for qualifying periods 1-3 and for 5-9.

The rules have also been loosened to increase the number of employers who may qualify. This has been accomplished through the following changes:

- Eliminating the revenue decline threshold requirement (30% for most periods) and allowing any eligible business experiencing a decline in revenue to qualify;

- Improving access for wages paid to certain employees who previously did not qualify, including:

- Certain non-arm’s length employees (e.g. the owner-manager) who did not receive remuneration during January-March 2020, and

- Employees that received no remuneration for 14 or more days in the qualifying period;

- Specifically including certain employers that previously did not qualify, including:

- those that have made business acquisitions through asset sales;

- those using third-party payroll providers (paymaster arrangements);

- those that have undergone amalgamations or windups; and

- those that could not qualify because they used the cash method of accounting (by allowing them to elect to use the accrual method).

There is also a safe harbour, or transitional rule, that applies in qualifying periods 5 and 6, which allows the employer to benefit from the old CEWS rules, if the subsidy would be higher than under the new rules. For those periods, the employer would calculate the wage subsidy under both the old rules and the new rules. The higher amount would be the employer’s wage subsidy for each period.”

Although it is easier to qualify for a wage subsidy under the revamped program, the rules have also become more complex. There is the potential for increased risk with the calculation of “qualifying revenues” for purposes of determining the amount of the subsidy, as each percentage decline could have an effect on the amount of subsidy being claimed. Because of this, employers should ensure their revenues are accurately reflected in order to reduce the risk of the CRA challenging the claim.

CEBA extension

The CEBA is the $40,000 interest-free loan program ($10,000 of which is forgivable) available to small businesses that meet certain requirements. The original deadline to apply for the CEBA was set at August 31, 2020. It has now been extended to October 31, 2020.

As an added benefit, the CEBA will be extended to businesses that operate through a personal bank account. Currently, only businesses that operate using a business bank account[1] are eligible to apply for the CEBA. Additional details are expected soon.

CECRA extension

The CECRA is the federal program that provides rent relief to commercial tenants who were experiencing financial difficulties and met certain other criteria. For landlords who apply on behalf of their tenants, the government covers 50% of the monthly rent and the landlord covers 25% of the monthly rent, leaving the tenant to pay only 25% of the rent for each month.

The program originally applied to the months of April, May and June. It was extended twice to include an opt-in for each of July and August. The government recently announced that it would extend the program by an additional month to include September. Additional details are expected soon.

Tax payment deadline extension

The federal government further extended the payment deadline for income tax amounts owing, as follows:

- Individuals (T1): 2019 tax balance due and instalments due on June 15 and September 15, 2020.”

- Corporations (T2): Balances due and instalments due on or after March 18 up to September 30, 2020.

- Trusts (T3): Balances due and instalments due on or after March 18 up to September 30, 2020.

The CRA has also stated that even though the filing deadline for corporations and trusts has not been extended further beyond September 1, 2020, they will not apply a late-filing penalty to corporations and trusts that file their return and make their payment by September 30, 2020.[2] Furthermore, no interest or penalties will apply on any tax debts up to September 30, 2020.

The CRA confirmed the relief from penalties and interest applies to all forms, elections and schedules that are tied to the return. This means common forms such as the T106 and T1135 also benefit from interest and penalty relief, provided they are filed by September 30, 2020.

New T4 reporting requirements

The federal government has introduced changes to T4 reporting requirements for 2020 that will be applicable to all employers. The purpose of these changes is to allow CRA to validate payments made under the CEWS, CERB and Canada Emergency Student Benefit (CESB).

In addition to reporting employment income in box 14 or code 71[3], employers will have to report the following amounts:

- Code 57: Employment income – March 15 to May 9

- Code 58: Employment income – May 10 to July 4

- Code 59: Employment income – July 5 to August 29

- Code 60: Employment income – August 30 to September 26

As an example: If an employer is reporting employment income for the period of April 25 to May 8, payable on May 14, code 58 should be used.

Home office expenses for employees

Many employees have been working from home throughout the pandemic, which has raised the question whether they should be entitled to a deduction for home office expenses incurred when calculating their income for 2020. Although this is still in the preliminary stages, CRA may allow employees who don’t normally work from home but have been forced to due to the pandemic to deduct home office expenses under certain circumstances. There are draft rules which are in the consultation stage, so nothing formal is currently available. If you have questions regarding the status of the consultation and what you’ll need to do as an employer, make sure to reach out to your advisor.

Changes to CERB

The CERB program has been extended to allow Canadians who qualify to access the CERB for an additional four weeks, up to a maximum of 28 weeks.

The CERB program is set to end on October 3, 2020. In response to the upcoming end to the CERB, the government is proposing the following changes:

- Temporary changes to the Employment Insurance program that will reduce the minimum number of hours needed to qualify, reduce the minimum regional EI rate to qualify to 13.1%[4] , and set a minimum EI benefit rate of $400 per week for new EI claimants as of September 27, 2020.

- Three new programs to replace the CERB:

- Canada Recovery Benefit: effective September 27, 2020. It would provide a benefit of $400 per week for up to 26 weeks to self-employed workers and those in the gig economy, who meet certain other requirements. If individuals return to work, they would still be able to continue to receive the benefit, although $0.50 would need to be repaid for every $1.00 of net income over $38,000 for the year.

- Canada Recovery Sickness Benefit: effective as of September 27, 2020 for one year. It would provide a benefit of $500 per week for up to 2 weeks for workers who meet certain criteria and are unable to work because they are sick or must self-isolate due to COVID-19.

- Canada Recovery Caregiving Benefit: effective as of September 27, 2020 for one year. It would provide a benefit of $500 per week for up to 26 weeks per household and is for individuals who meet certain criteria and are unable to work because they need to provide care for children or dependents who have to stay home.

Although the CERB extension to 28 weeks is now in place, the other changes mentioned above are still just proposals and require legislative approval to take effect. Any vote on these proposals will take place after September 23, once the House of Commons is in session.

[1] To qualify, under the current rules, the business must be using a business bank account that was opened with its primary financial institution on or before March 1, 2020.

[2] Corporations and trusts that would otherwise have a filing deadline on May 31, June, July or August 2020, originally had the filing deadline extended to September 1, 2020.

[3] Code 71 is used by employers paying tax-exempt remuneration to employees who have Indian status under the Indian Act.

[4] The regional EI rate is used to determine access to EI regular benefits, taking into consideration the level of unemployment in a given EI region. EI regions in Canada that have a higher rate than 13.1% will have it reduced to 13.1%, making it easier for individuals to qualify for EI. For EI regions with a lower rate than 13.1%, that lower rate will still apply.